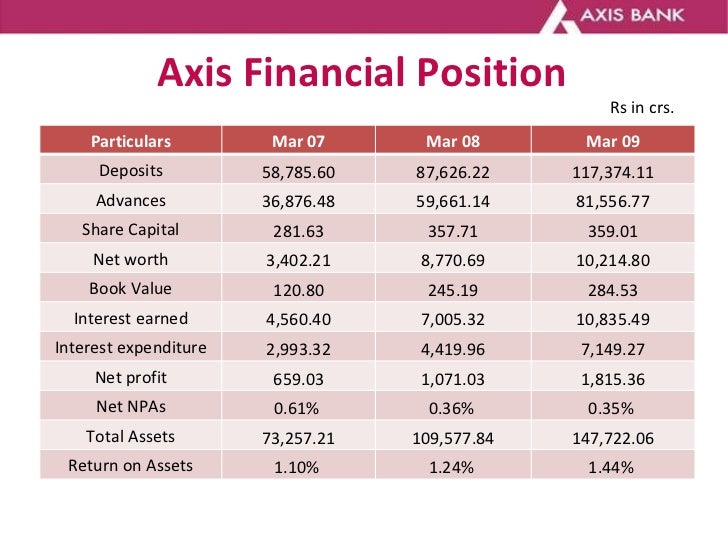

Table of Content

As a rule, your savings must cover the additional purchase costs. Depending on the state, this is between 9% and 12% of the purchase price of the property. The amount of equity required cannot be answered in general terms.

The more equity or savings you bring in, the lower your loan-to-value ratio LTV and hence the interest rate at which the bank grants you your mortgage. Typically, banks lower the interest rate gradually in 5% steps of the LTV. In other words, a higher down payment means a lower LTV and a lower interest rate, and vice versa, a lower down payment means a higher interest rate due to a higher LTV. A fixation period which is too short could cause you financial hardship if interest rates go up significantly in the future.

Mortgage Options include:

Our custom optimization engine and expert advisors will help you make the optimal decision for your personal circumstances. You can use the simple rent or buy calculator to evaluate if buying make sense for you. If the property to be mortgaged is a Condominium Property please refer legal department & address the same. Letter from the tenant to provide vacant possesion if the property is already occupied.

The repayment determines important conditions of your mortgage in Frankfurt am Main, for example, the repayment period and the monthly loan installment. In the case of an annuity loan, the monthly loan rate is made up of the interest portion and the repayment portion. In Germany, there are many mortgage lenders with different conditions and interest rates. The interest rates vary because banks calculate risks differently.

Why Commerce?

These fees are composed of the notary fee, real estate commission, and property transfer tax. In Frankfurt am Main, as in the rest of Germany, the equity you bring in should at least cover the purchase fees. If you only pay the purchase fees with your savings, means that you borrow the entire purchase price of the property from the bank. The amount of the down payment determines what is called the loan-to-value ratio .

Together with our team of experienced advisors, you will understand the nuances of your situation and fine-tune your mortgage decision. Mortgage rates have fallen sharply in recent years in Germany. While interest rates were around 6.5% in 2000, they have settled at around 1% in recent years. The low interest rates are a great advantage for buyers since the cost of the loan is rather low compared to the past and you can borrow money cheaply.

Log in to Online Banking or select an account:

“Simply put, my wife and I would not have our dream home without the help of LoanLink and Başar. Although our personal/financial situation was less than ideal, Başar was able to secure us an extremely favourable loan. I really doubt another broker could have done as well."

For us to find the optimal mortgage for you, we need to know your personal financial situation. We can help you with the financing you need to make your plans happen, and we'll do it with rates and payment terms that fit your needs. Most applications are approved the same day, and you can set up automatic payments from your checking account to make payback a snap.

You can also make an additional payment any time you wish. Use our mortgage calculators to see what your payment could be with today’s rates for a fixed-rate, ARM, Jumbo, FHA, VA, USDA and other home loan options. For a mortgage in Frankfurt am Main, the additional purchase costs are 10,98% or 8%, depending on whether you have to pay a real estate agent's commission or not. To feed the recommendation engine, we regularly review the mortgage products and conditions available in Germany, scouring over 750 lenders and their conditions on a daily basis. Unlike most brokers, we have integrated multiple banking platforms, which gives us the widest coverage in Germany. This is how we know exactly what is out there and can feed these conditions into the recommendation engine.

Copy of the receipt of the rates paid for the last quarter. Copy of the approved Building Plan (to purchase /construct a house). Any other documentary evidence to prove additional income.

The composition of interest and repayment changes slightly with each month. This is because each repayment reduces the remaining loan balance. To optimize the recommendation engine, we review daily the mortgage products and conditions of over 750 lenders. This is how we can understand exactly what offers are available and what conditions they have.

Once this information has been obtained, the file will be submitted for underwriting. Upon approval, your loan docs will be prepared locally, and you will close with the title company. There will be no disruption in service as your User ID and passwords will remain unchanged including your saved permissions and templates. You are leaving The Bank of Commerce's website and linking to a third party site.

In general, three factors influence the calculation of interest rates at the bank. These are, on the one hand, the mortgage itself and the situation of the borrower, and on the other hand, capital market conditions. The following example shows the difference between interest costs for a mortgage of 200,000 euros with a repayment rate of 2% and a 10-year fixed interest rate.

Fixed interest rateThe longer you fix the interest rate, the more security you have in planning your mortgage loan. However, you also have to accept higher costs, because the longer the fixed interest rate, the higher the interest rate that the bank will call. With a short fixed interest rate period, on the other hand, you benefit from a lower interest rate.

However, it is possible to take out a separate personal loan for this purpose. Furthermore, your monthly repayment should be calculated realistically, so you can easily cover it without having to restrict your accustomed standard of living. “We had a fantastic experience negotiating the complexities of the German banking system with Basar's help. We were able to secure a loan for even more than we expected with a fantastic rate and this was done quickly and with great customer service.

No comments:

Post a Comment